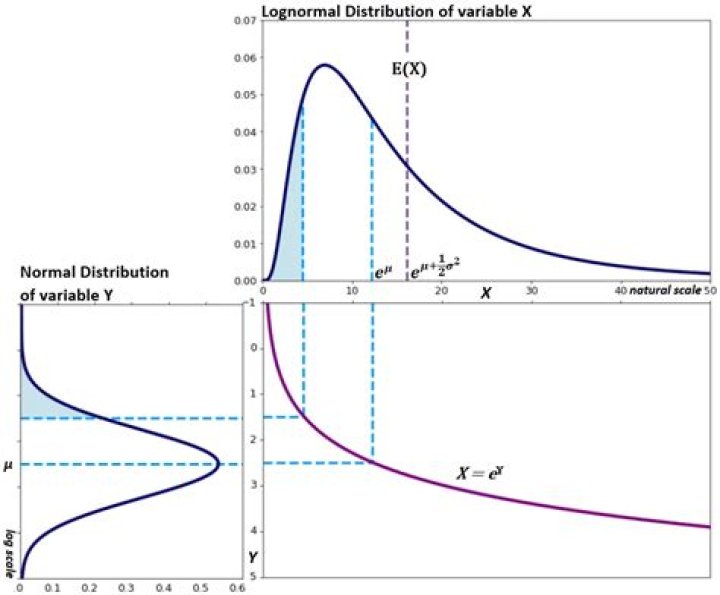

Expected value of a lognormal distribution [duplicate]

I'm having trouble deriving an expression for the expected value for the lognormal distribution. I've tried the standard approach of computing $\int_{\mathbb{R^+}}xf_X(x)\,\mathrm{d}x$ for non-negative variables:

$$\int_0^{\infty} \frac{1}{\sigma\sqrt{2\pi}}\exp\left(-\frac{1}{2}\left(\frac{\ln(y)-\mu}{\sigma}\right)^2\right)\,\mathrm{d}y$$

which is beyond me.

I've tried looking into moment generating functions, of which my knowledge is lacking, but stumbled upon a question claiming (and proving) that there is no such function. (link)

I've looked at a similar question (same, really) (link), but I'm afraid I don't undestand the accepted answer. It seems to relate the moment generating function of the normal distribution to the lognormal one, which didn't exist?

So how does one extract the expected value for the lognormal distribution, given the moment generating function of another(/the normal) distribution?

Bonus question: Is this last method the most natural approach (yes/no), or is it possible to find the expected value using the first approach with some clever trick (yes/no).

$\endgroup$ 62 Answers

$\begingroup$Standard method to find expectation(s) of lognormal random variable.

1)

Determine the MGF of $U$ where $U$ has standard normal distribution.

This comes to finding the integral:$$M_U(t)=\mathbb Ee^{tU}=\frac1{\sqrt{2\pi}}\int_{-\infty}^{\infty}e^{tu}e^{-\frac12u^2}du=e^{\frac12t^2}$$

2)

If $Y$ has lognormal distribution with parameters $\mu$ and $\sigma$ then it has the same distribution as $e^{\mu+\sigma U}$ so that: $$\mathbb EY^{\alpha}=\mathbb Ee^{{\alpha}\mu+{\alpha}\sigma U}=e^{{\alpha}\mu}\mathbb Ee^{{\alpha}\sigma U}=e^{{\alpha}\mu}M_U({\alpha}\sigma)=e^{{\alpha}\mu+\frac12{\alpha}^2\sigma^2}$$

$\endgroup$ 7 $\begingroup$Hint:

By the substitution $y=e^z$, you transform to

$$\frac{1}{\sigma\sqrt{2\pi}}\int_{-\infty}^{\infty} e^z\exp\left(-\frac{1}{2}\left(\frac{z-\mu}{\sigma}\right)^2\right)e^z\,\mathrm{d}z=\frac{1}{\sigma\sqrt{2\pi}}\int_{-\infty}^{\infty} \exp\left(-\frac{1}{2}\left(\frac{z-\mu}{\sigma}\right)^2+2z\right)\,\mathrm{d}z$$ which you can reduce to a standard Gaussian integral by shifing the variable, giving the value $1$.

$\endgroup$ 1