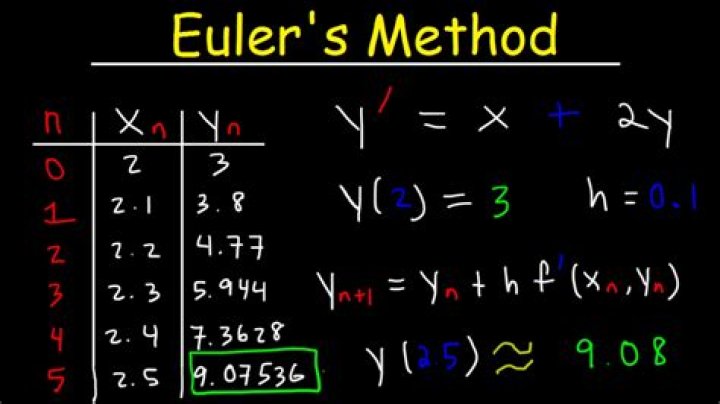

Euler Allocation Method

Herr Euler is so prolific that perhaps this has not been asked before. I read a paper - "Capital Allocation to Business Units and Sub-Portfolios: the Euler Principle Dirk Tasche" - showing a proof of the "EULER ALLOCATION METHOD" but after trying to follow it through it then referred to fuzzy logic game theory invented in the 50s by Shapley et al. On page 5 it refers: "Denault (2001) derived the Euler principle by game-theoretic considerations". Since Euler didnt have access to that, how did he come up with the concept. Its used to allocate VAR in risk. I think perhaps its just saying that is you have a lot of gradients making a continual surface then the average gradient is the natural allocation. Is there more to it than that? The article is by Dirk Tasche. (sic p5)

Theory

The Euler allocation principle may be applied to any risk measure that is homogeneous of degree 1 in the sense of Definition A.1 (see Appendix A for full or formula below) and differentiable in an appropriate sense. ...

(sic part of Appendix A.1)

Theorem A.1 (Euler’s theorem on homogeneous functions) Let U ⊂ Rn be an open set and f :U → $R^{n}$ be a continuously differentiable function. Then f is homogeneous of degree τ if and only if it satisfies the following equation:

$\tau f\left( u\right) = \sum ^{n}_{i=1}u_{i}\dfrac{\partial f\left(u\right)}{\partial u_{i}}$

$u=\left( u_{1},\ldots u_{n}\right) \in U, h>0$

$\endgroup$ 6 Reset to default